1. Introduction

Interest rate is one of the most important economic indicators for a nation, whichrepresents the price of capital, reflects supply and demand. It can not only reflect onecountry's capital market conditions, but also be able to influence on other economicindicators, such as GDP, investment, income and so on.Term structure depicts the relation between YTM for zero-coupon bond andmaturity (or called zero-coupon bond maturity yield curve). The shape of the curvecan be flat, upward, downward, or even more complicated. And all of them can reflectthe market situation. Term structure is widely applied in investment portfolio, assetpricing, risk management, monetary policy. Therefore term structure is a basicinstrument to portray interest rate.In China, there are many kinds of interest rate. Such as deposit and lending rates,the repo rate, the discount rate and so on. In finance, the most important one is therisk-free rate. It can not only provide the benchmark interest rate, but also be appliedin the financial instruments development.

According to the experience of other countries', YTM of Treasury bond is usedas the risk-free rate, because the government has the highest credit rating in order toensure that they are not likely to default. Moreover, it is widely traded in the market,and the price is determined by numerous investors, so it can reflect the real situation.Compared to Western developed countries, China's bond market started late, butdeveloped quickly. In 1991, Shanghai stock exchange started trading bond. In 1997,inter-bank market was set up which indicated that China has established a large andstandardized bond trading market for banks and financial institutes. And theinter-bank market trading volume is far greater than Exchange. Therefore, the studyfor the Treasury bond term structure will be more meaningful.

......

2. Literature Review

2.1 Term Structure

The traditional theory of the term structure basically consists of the followingthree theories:Expectation Hypothesis: Fisher (1896) proposes this hypothesis first; the maindevelopment of the theory is developed by Hicks (Hicks, 1946) and Lutz (Lutz, 1940).Malkiel (1966), Meiselman (1962) and Roll (1970, 1971) make the furtherimprovement of the theory. The pure expectations theory view expectations of futureinterest rates as an important factor to determine the current term structure. The YTMof long-term bond is the function of the expectation of the short-term bond YTM.Therefore, if expectation of short-term bond YTM is equal to YTM at that time, thenthe long term YTM is same as short-term ones, so curve will be flat. If investorsexpect the short-term YTM will go up, the curve will be upward.Liquidity Preference Theory: This theory is first proposed and analyzed byHicks (1946) and Kessil (1965) make the further supplement. Long-term debt burdengreater market risk, so investors will require compensation. Therefore long-terminterest rates are based on the expected interest rate plus compensation for the risk.Market Segmentation Theory: Culberrtson (1957) proposes that the bondmarket with different maturity is independent. Therefore the whole market issegmented by different term. The equilibrium is decided within its own market.However, because this theory assume different market is independent, it cannotexplain that different market sometimes move simultaneously, and also cannot explainthat the long-term interest rate will change regularly corresponding to the short-terminterest rate.The traditional theories are the foundation for the term structure, but they arehard to be quantified for Modeling.

.....

2.2 Principal Component of Difference Interest Rate

For term structure, we cannot use it directly, but just pick time series from thestructure with the same maturity and do the further research on them.There are a lot of different kinds of maturity, and each time series' informationmay overlap and have higher correlation. The number of the variables will increasethe complexity and difficulty of solving problem. And the higher correlation willcause the bias on the result.Principal component analysis is widely used to deal with many indicators andfind the general relationship between them.Through the principal component analysis, the principal components maintainthe most information the previous variables have, and the number of variables willdecrease. Each component has no correlation and is the linear combination ofprevious variables. According to the volume of the information the new componenthave, they can be sorted as first principal component, second principal component,etc.Litterman and Scheinkman (1991) use PCA to analyse the US zero coupon curveand find three principal components having significant influence on the yield tomaturity, and define them as level factor, slope factor and curvature factor can explain96% change of the term structure. D' Ecclesia and Zenios(1994), Buhler andZimmermann(1996) apply the PCA method to analyse the Italy, German and Swissterm structure, and find that the three components can explain nearly 99.4%and 94%of the change of the variance. In China, Zhu Shiwu (2003) uses the data fromShanghai Exchange (2002/4/19-2003/4/5) to find that three components can explain94% of the variance. Tang Gerong and Zhu Feng (2003) use the data from Shanghai Exchange (2001/8/30-2001/12/13) to find that they can explain nearly 90% of thevariance.

......

3. Empirical Study .....12

3.1 Sample.....12

3.2 Modeling ..........17

3.3 Analysis for the Result .......18

3.4 Principal Component Analysis....24

4. Analysis of Macro Factors .......27

4.1 Selection of Macro Factors .........28

4.2 Vector Auto Regression Model............34

5. Conclusion ....53

5.1 Term Structure Result ........53

5.2 Principal Component Analysis Result ..........54

5.3 Relationship between Interest Rate and Macro Factor....55

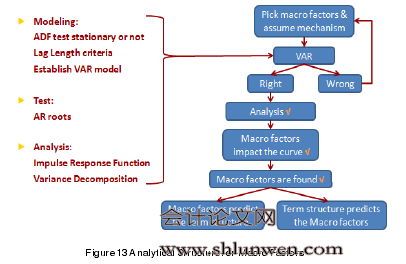

4. Analysis of Macro Factors

In the VAR model, we need to do the ADF test for each variable and checkwhether it is stationary. After that, VAR model can be established. When the VARmodel has been established, unit root test will be applied to check whether the VARmodel itself is stationary. If it is really stationary, we can do the following steps toexplore the important information from the model.Because the VAR model is not a theoretical model, so in the VAR model, thesisdoes not check the influence of one variable's change on another variable. Thesis needto use impulse response function to figure out that when an error makes change whatis its effect on the system.Variance decomposition is used to analyze the contribution of each impact on thechange of endogenous variable. Therefore, the variance decomposition can be used tocheck the contribution of one shock to the change of another variable.There are a lot of different kinds of indicators that can reflect the performance ofthe economy, but we needn't to pick all of them to analyse the relationship amongthem. According to our design, we need to select the macro factors that can representthe different participants in the economy. We conclude that in the interbank marketthere are four important roles: customers, government, traders and then enterprises.And we will apply CPI, M2, Trading Volume and PMI to represent the reaction ofeach party. And our goal is to find how they can affect the shape of the term structure.For the shape, according to the previous research, we can conclude them as threefactors: level, slope and curvature. All of them have been introduced and calculated inthe previous sector.

......

Conclusion

It needs to reflect the real economic situation. For example, except for somespecial case, the long-term interest rate should be higher than short-term interest rate.Term structure should represent the whole picture of the interest rate from themarket. Therefore it can filter the market occasional irrational movement, and reflectthe real or theoretical interest rate. So it should be smooth enough and cannot havemuch fluctuation. It is not meaningful that we make the term structure equal to thereal price but ignore the smoothness of the curve. However, sometimes the termstructure cannot meet both the precise and reasonable criteria.In the real world, the term structure needs to maintain stable, which means forthe several adjacent days the term structure should not change dramatically. And thiswill need the further adjustment.In China, bond market is still growing. Compared with developed market itdoesn't have enough samples to fit the curve, and the market is not well-regulated sothere is a lot of inside information. All of them will influence the accuracy of the termstructure.

............

References (omitted)